Why Your Car Insurance Goes Up After Someone Else Hits You (2026 Complete Guide)

Sam - The Chaos Aunt

11 min read

Prices verified March 2026

Includes Video

Nobody tells you that a 'not-at-fault' accident can still cost you 45% more on your insurance premium for three to five years. I found out when a distracted driver T-boned my 2018 Tacoma, and my rates still climbed by $35 a month.

★ Best Overall

Editor picks below — verified, expert-reviewed.

Nobody tells you that a 'not-at-fault' accident can still cost you 45% more on your insurance premium for three to five years. I found out when a distracted driver T-boned my 2018 Tacoma, and my rates still climbed by $35 a month. That's an extra $1260 over three years for someone else's mistake. It's a financial biohazard. Insurify reports these increases are standard.

The Short Answer

Your insurance company views any accident, even one where you're not at fault, as an elevated risk indicator. They don't care who's to blame; they care about the statistical probability of you filing another claim. You've demonstrated 'exposure' to incidents.

This isn't about justice. It's about data. Insurers are running a probability matrix, not a court of law. If you've been in one accident, even if it wasn't your fault, their algorithms flag you as statistically more likely to be involved in future incidents. Progressive states this directly: any claim can increase your rate.

Think of it as a threat assessment. Your driving record is your tactical dossier. A clean record means low threat. An accident, even a fender-bender where you did nothing wrong, adds a 'threat marker.' It indicates you operate in a high-traffic zone where incidents occur.

They're not punishing you. They're re-evaluating their own potential payout. Your vehicle's repair costs, medical claims from passengers, or even just the administrative overhead of processing a claim all factor into their risk assessment. This isn't personal; it's actuarial.

Some states allow insurers to raise rates for not-at-fault accidents. Your state's regulatory environment dictates how much they can squeeze you. This isn't universal, but it's common enough to be a critical planning factor. Car and Driver confirms that a history of claims, regardless of fault, can trigger rate increases.

Your 'risk profile' has been updated. This new profile suggests a higher potential for future claims, even if those claims are also not your fault. It's a brutal logic, but it's the operational reality of the insurance industry. They're managing their own financial biohazard.

This re-evaluation impacts your 'underwriting group.' You move from one risk category to another, and the new category comes with a higher premium. Quora discussions highlight this group re-categorization. It's not about what you did, but what the data suggests you might cost them.

It's a statistical debrief. They look at the total cost of claims in your area, the rising cost of parts, and then your personal involvement in any incident. All these variables feed into the new premium calculation. Your exposure means you're now part of a more expensive risk pool.

Insurance rates can be influenced by various factors including your credit score, as detailed in our article on how credit scores affect rates.

The Reality Check

A 'not-at-fault' incident can trigger a 10-20% premium hike, even without a ticket. This isn't a penalty for your driving, it's a recalibration of your 'exposure' to risk. The system sees you as being in the wrong place at the wrong time, more frequently. Selectsource Insurance explains this 'crystal ball of risk' phenomenon. Consider the rising cost of parts. A simple fender-bender on a late-model SUV can involve replacing sensors, cameras, and intricate body panels. A $1000 repair 10 years ago is now a $3500 job. This increased cost of claims across the board affects everyone's rates, including yours. Progressive notes that general claim costs in your ZIP code impact rates. Even if you have accident forgiveness, it's usually for your first *at-fault* accident. A not-at-fault claim can still ding you. Some insurers offer 'minor accident forgiveness' but that's a specific add-on, not a standard feature. Always check your policy's fine print. Ainvest details accident forgiveness as a key protection. Your 'claim frequency' matters. One not-at-fault accident might be a blip. Two in two years, even if neither were your fault, makes you a statistical magnet for trouble. Insurers see a pattern, not individual events. InsuranceQuotes confirms claim frequency is a major factor.| Component | How It Fails | Symptoms | Fix Cost |

|---|---|---|---|

| Bumper Cover | Minor impact, cracking plastic | Visible cracks, paint damage | $800 - $1500 |

| Headlight Assembly | Bracket damage, internal wiring break | Dim/flickering light, moisture inside | $400 - $1200 |

| Fender Panel | Creasing, paint chipping, alignment issues | Visual distortion, door misalignment | $600 - $1800 |

| Wheel Alignment | Impact to suspension components | Steering pull, uneven tire wear | $100 - $300 |

Understanding these insurance implications can be crucial, so be sure to follow our checklist for car accidents.

How to Handle This

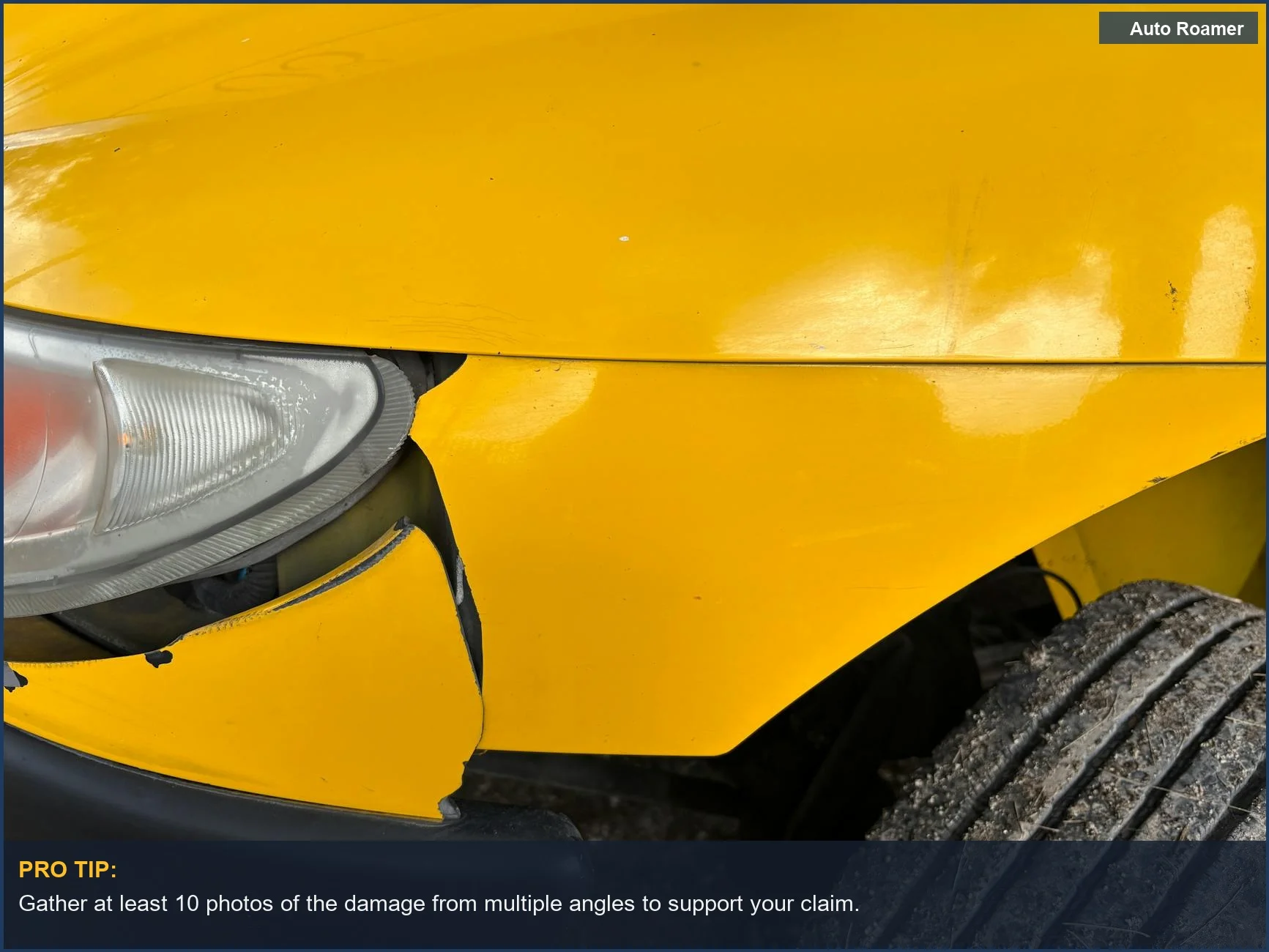

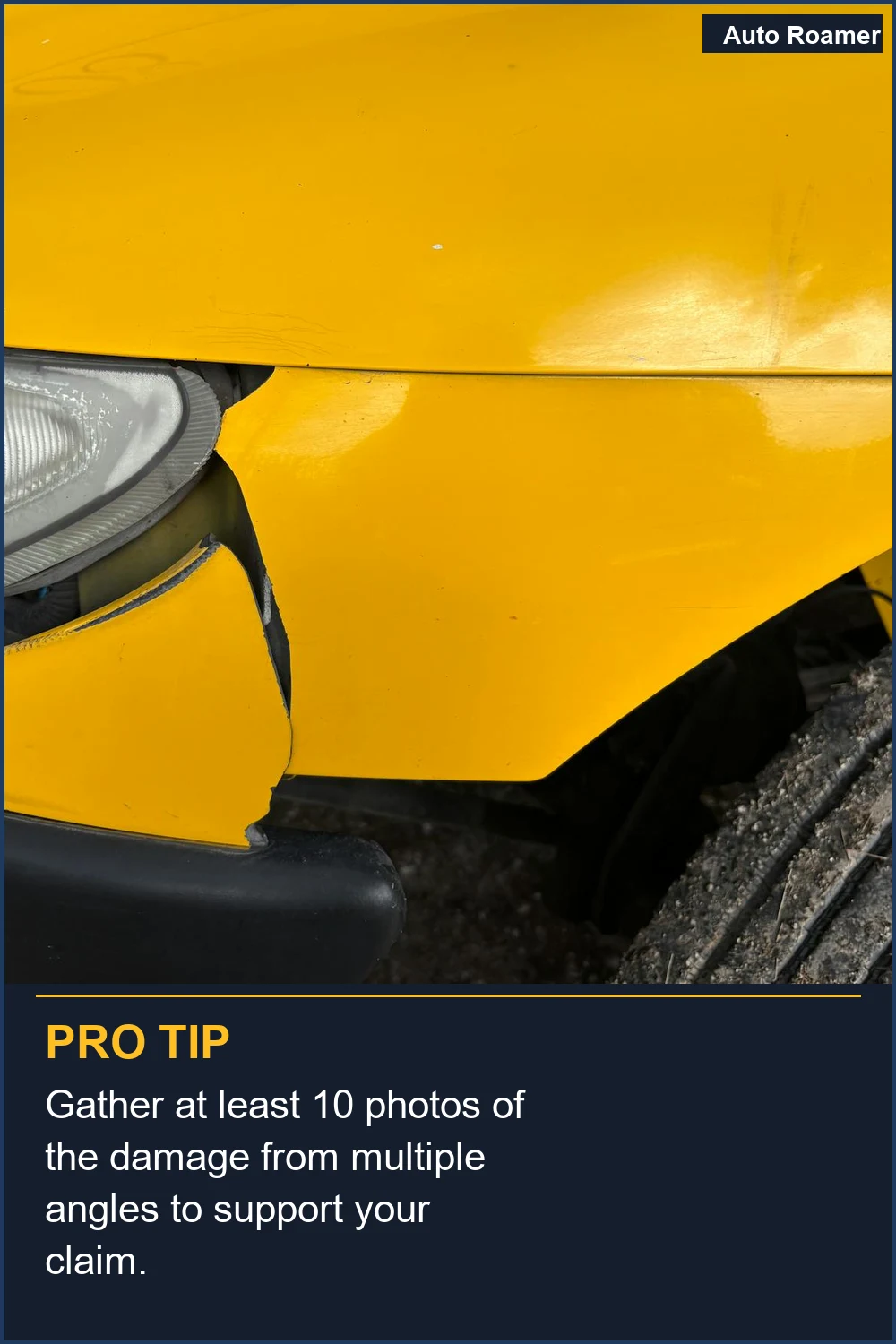

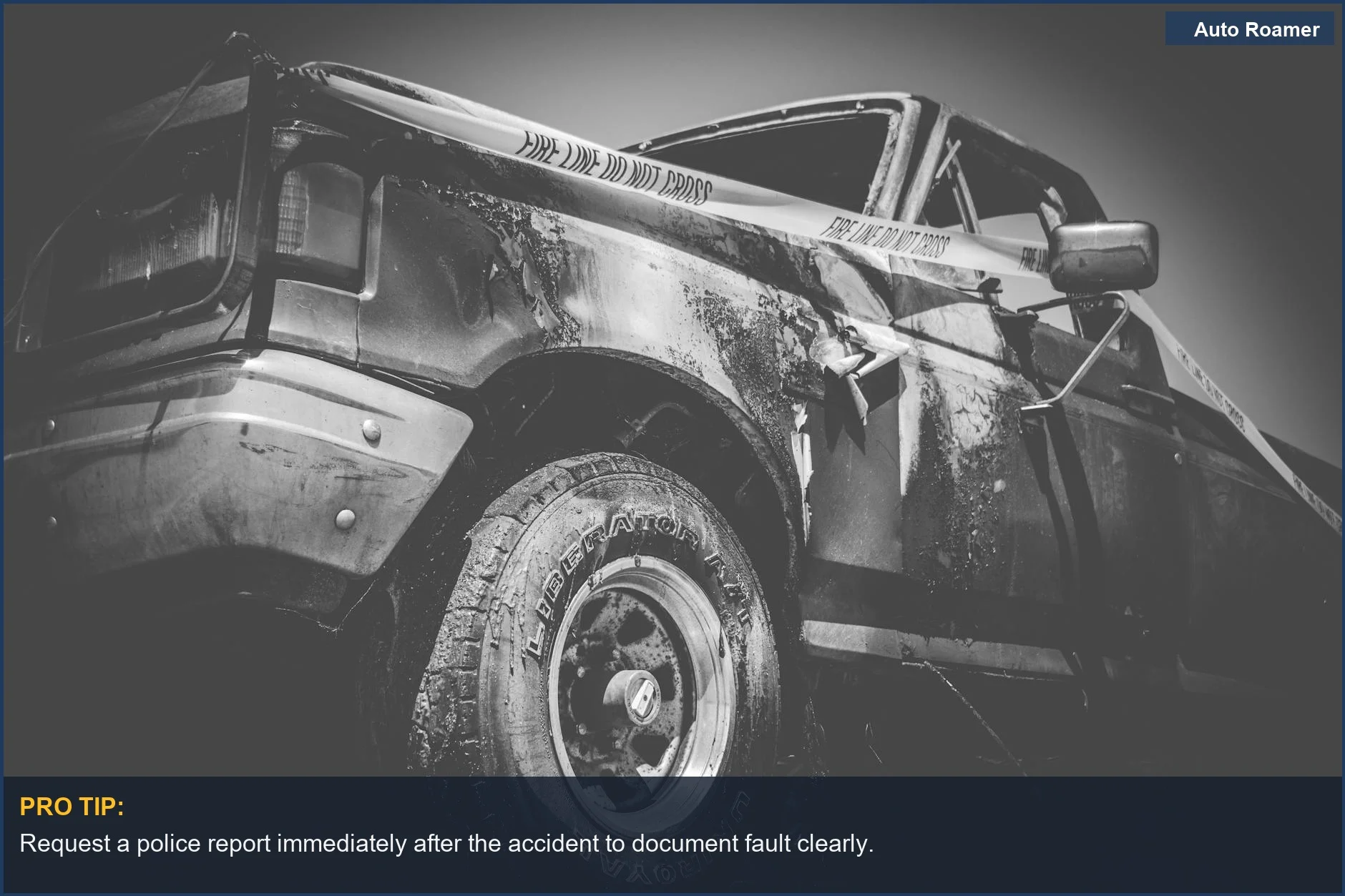

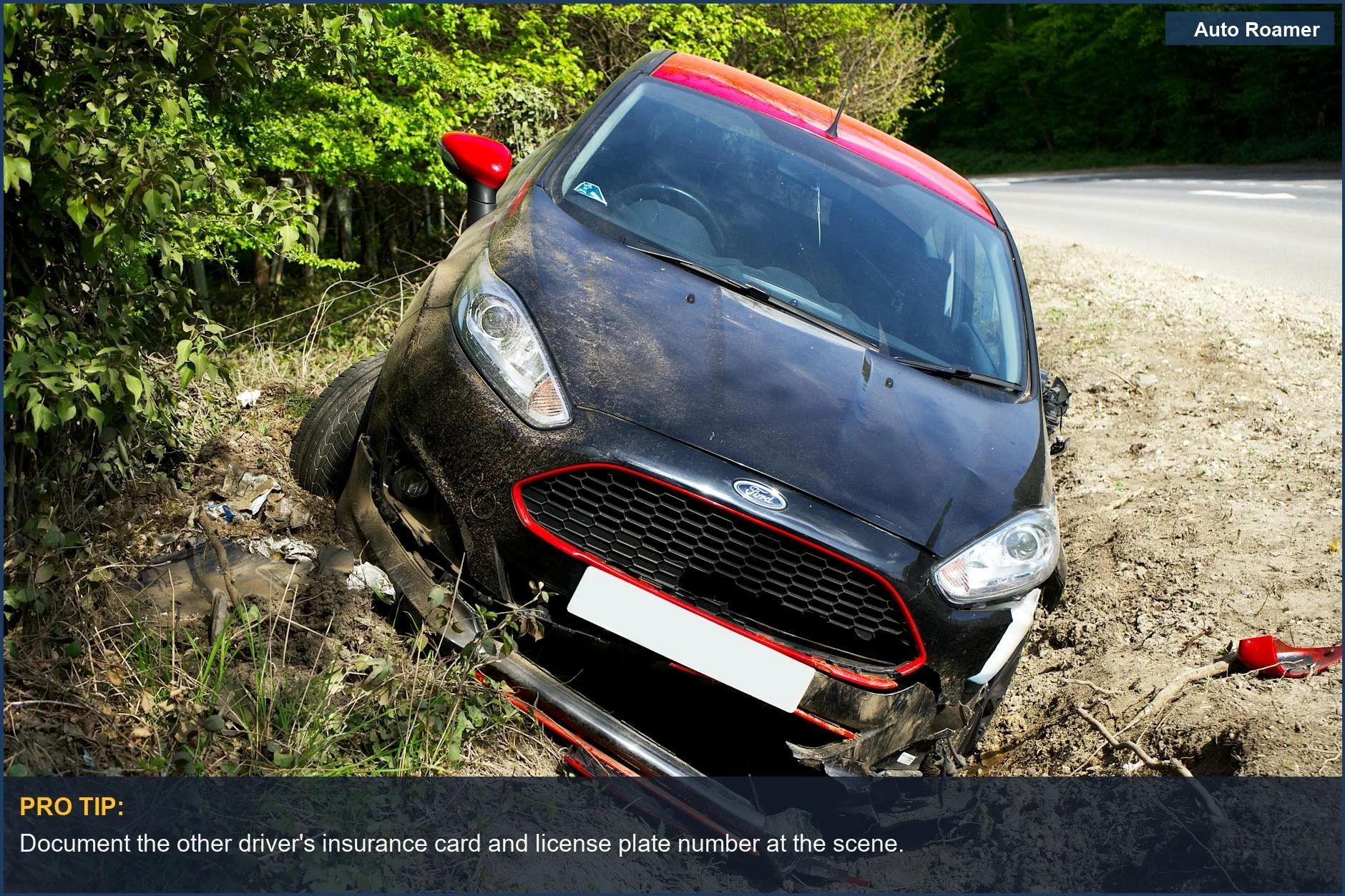

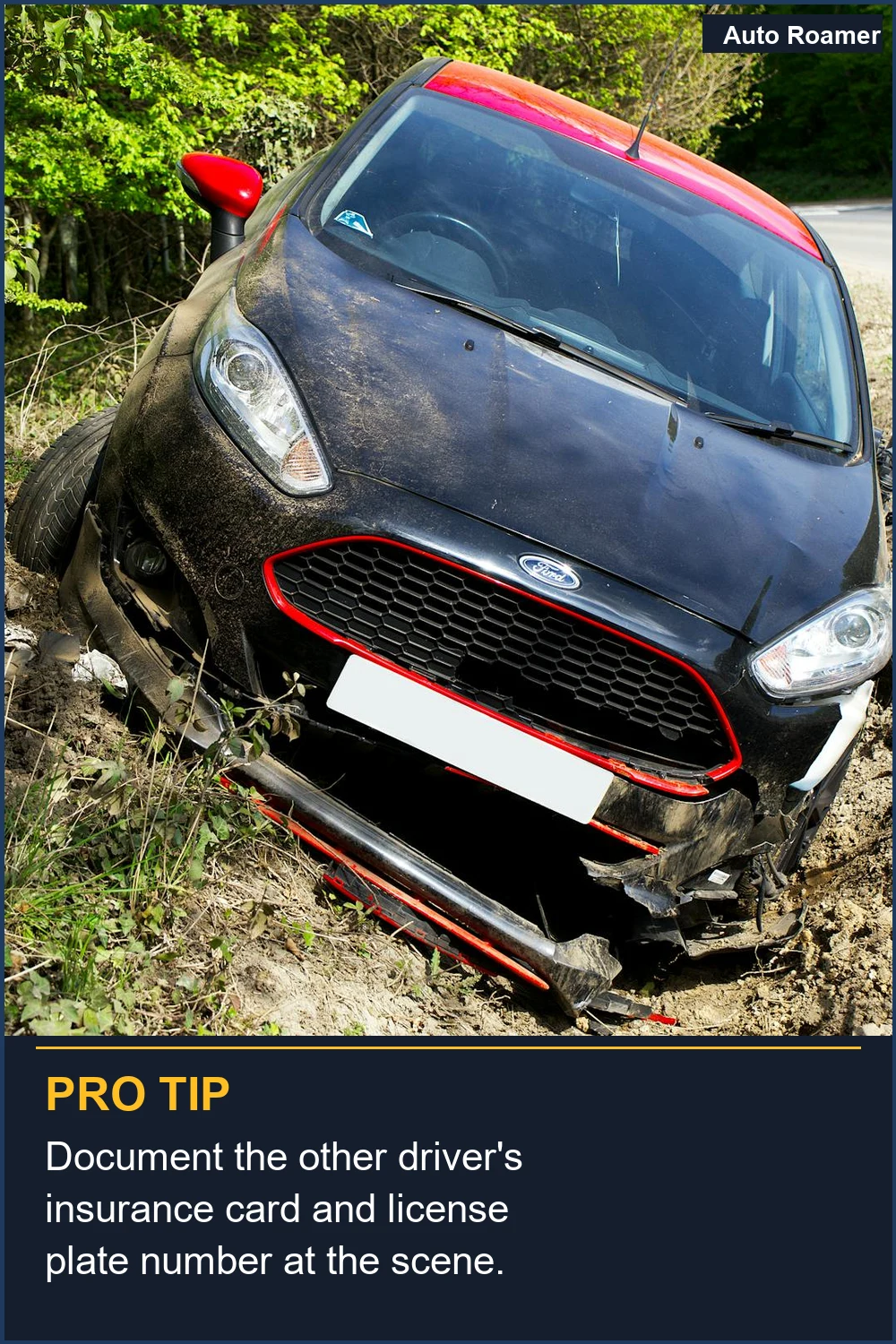

1. Document EVERYTHING at the scene: This is your primary intelligence gathering. Get 10-15 photos from multiple angles of both vehicles, license plates, and the other driver's insurance card. Note the exact time, date, and intersection. This is your immediate hazmat containment. 2. Call the Police for a Report: Even for minor fender benders. A police report is an official, third-party assessment of fault. Without it, it's your word against theirs, and that's a logistical nightmare. This report is critical for your extraction protocol. Quora advises on the importance of this. 3. Notify Your Insurer IMMEDIATELY: Even if you don't plan to file a claim with them. They need to know the incident occurred. This preempts the other party's insurer from contacting them first with a potentially skewed narrative. This is your initial damage control. 4. Get an Independent Repair Estimate: Don't just go with the body shop your insurer recommends. Get two or three estimates. This gives you leverage and a clearer picture of the actual repair cost, which is crucial for deciding whether to file through your own policy. A $700 repair might not be worth a $300 annual premium hike. 5. Understand Your State's Rules: Some states prohibit rate increases for not-at-fault accidents. Know your rights. This is your regulatory survival guide. If your state allows it, prepare for the financial impact. AAA acknowledges that accidents don't automatically raise rates. 6. Review Your Policy's Accident Forgiveness: If you have it, confirm it applies to not-at-fault incidents or if it's only for your first at-fault crash. This is a critical sanity-saver if applicable. Don't assume. Ainvest highlights accident forgiveness as a policy add-on. 7. Shop Around at Renewal: If your rates jump, don't just accept it. Get quotes from 3-5 other insurers. Your new 'risk profile' might be assessed differently by a competitor. This is your tactical redeployment. Insurify suggests comparing rates to find better deals. 8. Consider Your Deductible: If the damage is minor, say $800, and your deductible is $500, filing a claim might only net you $300. That small payout could trigger a multi-year premium increase that far exceeds the benefit. This is a crucial cost-benefit analysis. Sometimes, out-of-pocket is the better long-term survival strategy.

Understanding your credit score can also help you navigate how smart car technology influences insurance costs.

What This Looks Like in Practice

Scenario 1: You're rear-ended on I-70 by a distracted driver. Police report clearly states they're at fault. Your 2020 Honda Civic has $2,200 in bumper damage. Your premium increases by $15/month ($180/year) for three years, totaling $540. The insurer sees you as being 'exposed' to high-speed rear-end incidents. Baldwin insights mention that damage to others can cause increases. Scenario 2: A deer jumps out, you swerve, hit a guardrail. No other cars involved. Comprehensive claim for $3,500 in body damage to your 2019 F-150. Your premium rises $20/month ($240/year) for five years, totaling $1,200. Animal collisions, while not 'at-fault,' still increase your perceived risk of future comprehensive claims. InsuranceQuotes states comprehensive claims can raise rates, but less than at-fault collisions. Scenario 3: Someone dings your parked car in a lot and leaves a note with their insurance. Minor scrape, $600 repair to your 2021 RAV4 door. You file with their insurance. Your own insurer still raises your rate by $8/month ($96/year) for two years. This is your 'claim frequency' marker. They see you as having a higher probability of needing future repairs, even if you weren't driving. Car and Driver explains a history of claims can raise rates. Scenario 4: You hit a pothole that blows out a tire and bends a rim on your 2017 Subaru Outback. $750 repair. You file a collision claim (even though it's a single-vehicle incident, it's usually processed as collision). Your premium goes up $25/month ($300/year) for three years. This is an 'at-fault' incident in the eyes of the insurer, even if you blame the road. Your tactical error was hitting the hazard. Scenario 5: Your car is stolen. Comprehensive claim for $25,000 for your 2022 Kia Forte. Your premium increases $10/month ($120/year) for three years. While not your fault, you're now in a higher-risk category for theft. Your vehicle location is a factor in this new risk profile. Selectsource Insurance explains that any accident is seen as an increased risk profile. Scenario 6: A hail storm totals your 2015 Chevrolet Silverado. $12,000 comprehensive claim. Your premium increases by $12/month ($144/year) for two years. While weather is uncontrollable, living in a hail-prone area means you're statistically more likely to file another comprehensive claim. This is a location-based threat level assessment.

If you ever find yourself in a minor accident, knowing what to do afterwards can be crucial.

Mistakes That Cost People

| Mistake | Consequence | Mitigation |

|---|---|---|

| Not calling the police | No official fault determination; 'he said/she said' scenario. Your insurer might assign partial fault to avoid payout. | Always get a police report, even for minor incidents. It's your primary evidence. |

| Not documenting the scene | Lack of visual evidence; makes it harder to prove the other party's negligence. Your claim could be denied or delayed. | Take 10+ photos/videos of all vehicles, damage, road conditions, and signs. |

| Admitting fault (verbally) | Any admission, even an apology, can be used against you by the other insurer. Never say 'my fault.' | Only exchange information. State facts, not opinions or apologies. |

| Not getting multiple repair estimates | Accepting the first quote without verifying market rates. You might overpay or miss cheaper options. | Get 2-3 estimates from different reputable shops. Compare parts and labor. |

| Filing a claim for minor damage | A $600 claim on a $500 deductible might net you $100 but trigger a multi-year premium hike far exceeding that. | Calculate the net payout vs. potential multi-year premium increase. Sometimes, paying out of pocket is cheaper. InsuranceQuotes discusses when to pay out of pocket. |

| Not shopping for new insurance at renewal | Staying with an insurer that has raised your rates unnecessarily. You're accepting their new, higher risk assessment. | Get 3-5 quotes from different companies every 1-2 years, especially after any incident. Insurify recommends comparing policies. |

| Assuming 'accident forgiveness' covers everything | Many policies only cover your *first* at-fault accident. A not-at-fault claim or a second incident might still raise rates. | Read your policy's specific terms for accident forgiveness. Confirm what it actually covers. |

Understanding the mistakes that can raise your insurance rates also highlights how your car might be selling driving data without your knowledge.

Key Takeaways

Your insurance rates can climb after a not-at-fault accident. This isn't personal, it's statistical risk assessment. Prepare for it.

In addition to accidents involving other vehicles, understanding what to do if you hit a deer can also impact your insurance rates, so be prepared with our guide on hitting a deer.

Frequently Asked Questions

My bumper cover got a crack, quoted $900 by the body shop. Can I just buy a used one for $250 and paint it myself to avoid a claim?

Yes, absolutely. A new painted bumper cover can run $800-$1500 installed. A used, unpainted one for $250 means you're out $250 plus $100 for a decent paint match kit. That's a $350 out-of-pocket vs. a potential $1000+ premium hike over three years. This avoids a claim entirely, preserving your clean record. It's a smart tactical move to prevent a financial biohazard.

Do I really need a dash cam? I've never been in an accident.

You don't 'need' it until you do. A 4K dash cam with front and rear views costs $150. That's your indisputable, real-time evidence of who initiated contact. Without it, your 'not-at-fault' claim becomes a 'he said, she said' scenario, which can take 45 days to resolve and still result in a premium hike. It's a critical piece of field-tested load-out for any serious driver.

What if I file a claim for a not-at-fault accident, my rates go up, and then I switch companies? Will my old claim still follow me?

Yes, your claims history follows you like a bad smell. Insurers access databases like CLUE (Comprehensive Loss Underwriting Exchange). That not-at-fault claim will be visible for at least five years, sometimes longer. Switching companies might get you a slightly better rate initially, but that claim is still a threat marker in your dossier, impacting future premiums. There's no escaping the data.

Can too many not-at-fault claims get my policy canceled?

Yes. While one or two not-at-fault claims usually just raise your premium, a pattern of three or more within a short window (18-24 months) can flag you as an 'unprofitable risk.' Insurers might non-renew your policy. You're not at fault, but you're a claims magnet. They'll drop you to reduce their exposure to what they perceive as a statistical biohazard. This is a severe long-term consequence of high exposure.

My friend said if I don't report a minor fender bender, my rates won't go up. Is that true?

Your friend is a liability. If the other driver reports it and you don't, you're now 'uncooperative' and 'at-fault by omission.' That's a 100% guaranteed rate hike, plus potential legal issues. Always report. You have 24-72 hours to notify your insurer, depending on the policy. Ignoring a potential biohazard doesn't make it disappear; it just makes it worse.

🏅 Looking for Gear Recommendations?

Check out our tested gear guides for products that work with this setup:

Sources

- What's happening with car insurance rates in 2026? - Facebook

- How Much Car Insurance Rates Go Up After an Accident - The Zebra

- Why did my car insurance rate go up? - Progressive Insurance

- Car Insurance After an Accident: The Real-World Guide for 2026

- Why Did My Car Insurance Rate Go Up for a Not at Fault Accident?

- Will My Insurance Go Up If Someone Hits Me? - Car and Driver

- cluballiance.aaa.com

- How Much Does Car Insurance Increase After an Accident? (2026)

- How New Claims Affect Your Car Insurance Premiums (2026 Guide)

- Why does my auto insurance raise my rates when the other car hit me?

- How Much Does Car Insurance Increase After An Accident?